| | Introduction | What does the retail sales data show? | What the Nielsen Global Consumer Survey on Snack tells us about snacking?| International market trends| What does this mean? | Source

,

Introduction

The snack market in Canada is rife with opportunities. A huge market size and increasing imports of snack foods create opportunities for Canadian and Alberta food manufacturers. Despite the market size, consumers are still demanding more from their snacks - accessibility, affordability and portability. There are opportunities to replace some of the imported snacks with� products made locally. In this issue, a brief overview of consumer trends on snack food products is provided to help Alberta food manufacturers gain insights into the market opportunities.

The North American Industry Classification (NAIC) defines snack foods as an industry comprised of establishments that are primarily engaged in:

- salting

- roasting

- drying

- cooking or canning nuts

- processing grains or seeds into snacks

- manufacturing peanut butter

- manufacturing potato chips, corn chips, popped popcorn, hard pretzels, pork rinds and similar snacks

The snack food industry is served primarily by domestic manufacturers. However, recently domestic market share is now being lost to imports. Canada’s snack food imports have grown by about 75 per cent from $384.6 million to $674.2 million between 2010 to 2014. In Alberta, the import value of snack foods has increased by $43.2 million during the same period.

Nielsen Market Research has estimated that traditional snack food sales in Canada from September 2013 to September 2014 through main retail channels at roughly $4.9 billion. Traditional snacks are defined as small portions of food or drink or light meals, especially those eaten between regular meals. In today’s fast-paced world, many consumers are blurring the line between a snack and a regular meal.� Market research in this area shows that changing lifestyles are redefining the way that we eat. Health, convenience, ease of use, variety and portability are all important attributes that consumers are looking for in their snack foods. If the definition is expanded to reflect all “snacking” the potential market would be worth $12.6 billion (Nielsen, 2014).

What Does the Retail Sales Data Show?

- Dollar sales of snacks in Canada rose four per cent in the 52 week period ending June 2014.

- Best-selling snacks included chips and cookies.

Source: Nielsen Market Track, National All Channels +Convenience and Gas (C&G ) – 52 week period ending September, 2014

- Candied snacks, meat sticks, fruits and nuts were among the fastest growing categories.

- Marketing opportunities exist in the segments with higher per cent growth in sales for confectionery, salty snacks, fruits and nuts and, dips and salsa.

Source: Nielsen Market Track, National All Channels +Convenience and Gas (C&G) – 52 week period �ending September, 2014

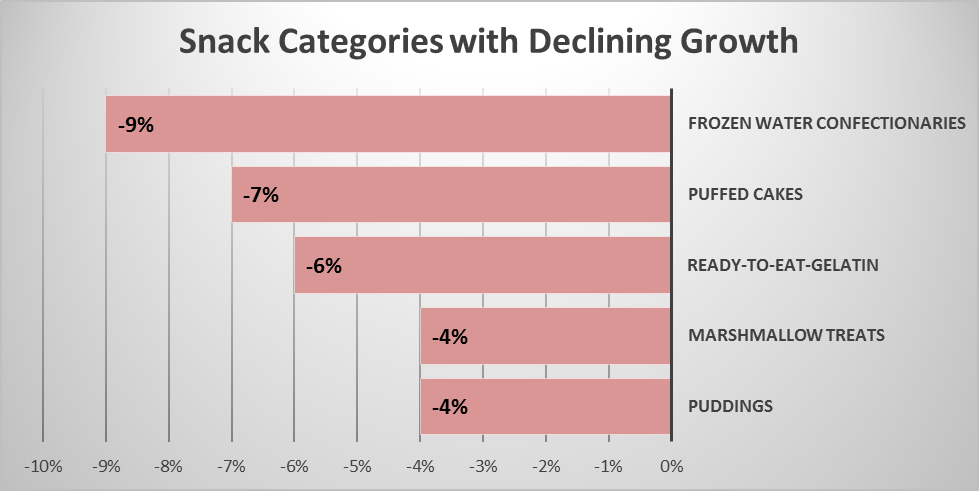

- Frozen water confectionaries, puffed cakes and ready-to-eat gelatine sales were categories on the list showing declining growth.

Source: Nielsen Market Track, National All Channels + Convenience and Gas (C&G) – 52 week period ending September, 2014

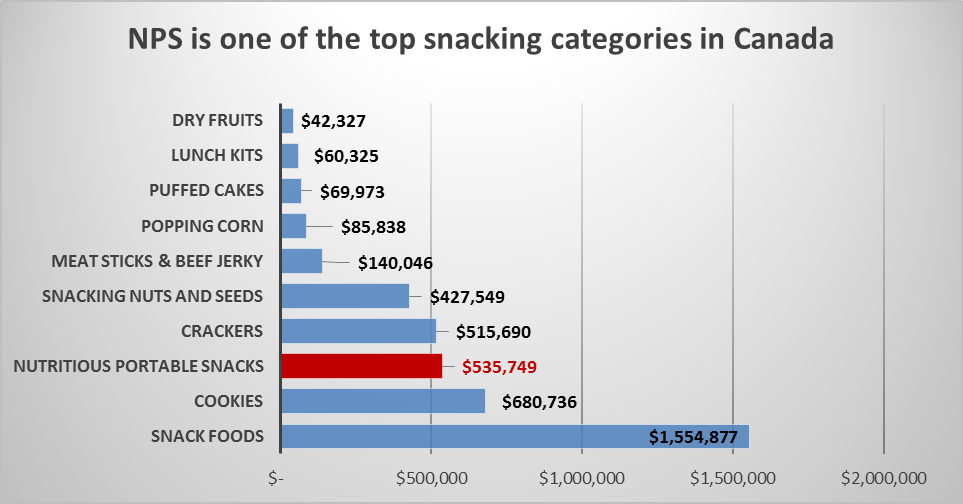

- According to Canadian Grocer’s publication Category Captain, the most recent data indicates that�consumers are particularly attracted to the convenience of Nutritious Portable Snacks (NPS) as well as the taste and perceived health benefits of these products.

Source: Nielsen Market Track, National All Channels +Convenience and Gas (C&G) – 52 week period ending September 2014 ending September, 2014

What the Nielsen Global Consumer Survey on Snack tells us about snacking?

- The average Canadian consumer enjoys 12 different types of snacks in a 30 day period.

- Chips, chocolate and fruit top the list of Canada’s favourite snacks.

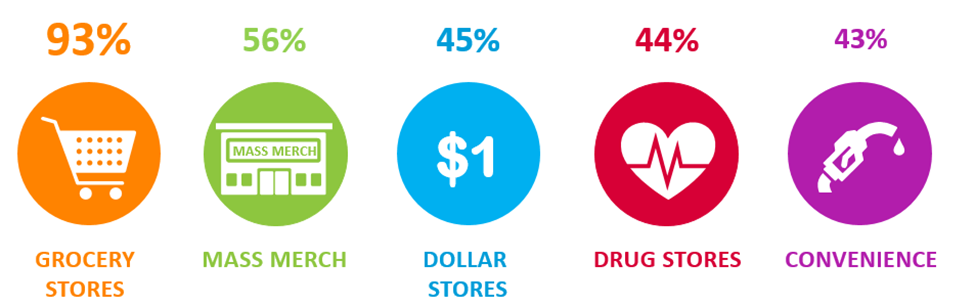

- Grocery stores remain the top destination for snack purchases.

Where people get their snacks (sometimes or often)?

- Four out of ten Canadians use snacks as a meal replacement.

- More than three thirds of the survey respondents want their snack ingredients to be local, organic and sourced sustainably.

- When consumers are snacking with a conscience, health attributes are very important to them. These attributes include; low salt/sodium, low sugar/sugar free, low calories, small portion sizes, high in fibre, whole grain and high in proteins.

- As consumers age they tend to look for healthier snacks. Meanwhile, younger consumers, under 35, are substituting breakfast and lunch with snacks.

- Younger consumers mostly snack on chocolate and chips while older consumers snack on fruits and cheese.

- Females tend to snack more than males. Males lean towards salty snacks while females seem to prefer sweet snacks.

Top five snacks consumed by males and females

Male | Female |

Chips | 65% | Fruit | 72% |

Chocolate | 61% | Cheese | 69% |

Cookies | 57% | Chocolate | 65% |

Sandwiches | 57% | Chips | 64% |

Cheese | 56% | Cookies | 59% |

Source: Nielsen Global Survey – Q1 2014 Canada

- Male shoppers are often overlooked in this market segment, but they account for 24 per cent of the�� primary shoppers.

- Canadian households with millennials will lead in spending on consumer packaged goods (CPG) by 2020. Since snack foods are the most commonly found CPG in millennials’ shopping basket, one might expect to see increasing spending on snack foods in the years ahead.

International Market Trends

An on-line survey conducted by the Nielsen in early 2014 found that within one year (March 2013 to March 2014) there was a two per cent sales growth in snack foods worldwide that was valued at US $374 billion. Some important findings include:

- North America and Europe are the biggest snack markets, worth US $124 billion and US $167 billion respectively.

- The fastest growing snack markets are in developing regions.

- During the year March 2013 to March 2014, snack sales in Latin America was up nine per cent to US $30 billion, the Middle East and Africa were up five per cent to US $7 billion and�Asia-Pacific was up four per cent to US $46 billion.

- As one might expect, snack preferences vary around the world. For instance, in North America, salty snacks comprise a fifth of all snack sales, while in Latin America cookies and snack cakes make up one quarter of all sales.

- By far the biggest snack category in Europe is sugary sweets such as chocolate, hard candy and gum.

- The most important snacks to watch are those with the fastest sales growth. Non-sugary snacks are closely aligned with meal replacement food and show a strong growth.

What Does This Mean?

When assessing opportunities, consider:

- The long term outlook for both domestic and �international snack food market is positive.

- There are generational shifts in snack food purchases. The main driver for millennials is Indulgence, while for boomers it is health.

- Consumers are demanding variety, innovation, accessibility and� portability in their snack purchases.

- Busy lifestyles often dictate a need for quick meals. While many opt for fast foods, others search for meal replacements.

- There is an opportunity to gain market share in the nutritious, portable and easy-to-eat meal alternatives that domestic snack food manufacturers could fill.

Source

Nielsen Market Track, National All Channels + C&G (Convenience and Gas) 52 weeks ending September, 2014 |

|